Canadian home sales edge up again in October

Ottawa, ON, November 15, 2017 – According to statistics released today by The Canadian Real Estate Association (CREA), national home sales posted a modest monthly increase in October but remain below levels recorded one year ago.

Highlights:

- National home sales rose 0.9% from September to October.

- Actual (not seasonally adjusted) activity stood 4.3% below last October’s level.

- The number of newly listed homes edged back by 0.8% from September to October.

- The MLS® Home Price Index (HPI) was up 9.7% year-over-year (y-o-y) in October 2017.

- The national average sale price climbed by 5% y-o-y in October.

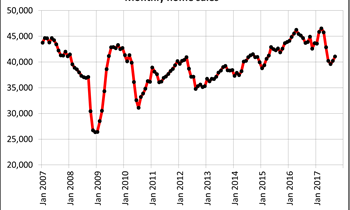

Home sales via Canadian MLS® Systems edged up 0.9% in October 2017 on the heels of monthly increases in August and September, but remained almost 11% below the record set in March. (Chart A)

Home sales via Canadian MLS® Systems edged up 0.9% in October 2017 on the heels of monthly increases in August and September, but remained almost 11% below the record set in March. (Chart A)

Activity in October was up from the previous month in about half of all local markets, led by the Greater Toronto Area (GTA) and the Fraser Valley, together with a number of housing markets in the Greater Golden Horseshoe region.

Actual (not seasonally adjusted) activity was down 4.3% in October 2017, extending year-over-year declines to seven consecutive months. Sales were down from year-ago levels in slightly more than half of all local markets, led overwhelmingly by the GTA and nearby cities.

“Newly introduced mortgage regulations mean that starting January 1st, all home buyers applying for a new mortgage will need to pass a stress test to qualify for mortgage financing,” said CREA President Andrew Peck. “This will likely influence some home buyers to purchase before the stress test comes into effect, especially in Canada’s pricier housing markets. A professional REALTOR® is your best source for information and guidance in negotiations to purchase or sell a home during these changing times.”

“National sales momentum is positive heading toward year-end,” said Gregory Klump, CREA’s Chief Economist. “It remains to be seen whether that momentum can continue once the recently announced stress test takes effect beginning on New Year’s day. The stress test is designed to curtail growth in mortgage debt. If it works as intended, Canadian economic growth may slow by more than currently expected.”

The number of newly listed homes eased by 0.8% in October following a jump of more than 5% in September. The national result was influenced most by declines in new supply in London-St. Thomas, Calgary and Greater Vancouver.

With sales up slightly and new listings having eased, the national sales-to-new listings ratio rose to 56.7% in October from 55.7% in September. A national sales-to-new listings ratio of between 40% and 60% is generally consistent with a balanced national housing market, with readings below and above this range indicating buyers’ and sellers’ markets respectively.

That said, this rule of thumb varies among local markets. Considering the degree and duration that current market balance is above or below its long-term average is a more sophisticated way of gauging whether local housing market conditions favour buyers or sellers. (Market balance measures that are within one standard deviation of the long-term average are generally consistent with balanced market conditions).

Based on a comparison of the sales-to-new listings ratio with its long-term average, about 60% of all local markets were in balanced market territory in October 2017.

The number of months of inventory is another important measure of the balance between housing supply and demand. It represents how long it would take to liquidate current inventories at the current rate of sales activity.

There were 5 months of inventory on a national basis at the end of October 2017, unchanged from the previous 2 months and almost on par with the long-term average.

At 2.5 months, the number of months of inventory in the Greater Golden Horseshoe region is up sharply from the all-time low of 0.8 months reached in February and March. However, it remains below the region’s long-term average of 3.1 months.

The Aggregate Composite MLS® HPI rose by 9.7% y-o-y in October 2017, representing a further deceleration in y-o-y gains since April and the smallest increase since March 2016. (Chart B)

The Aggregate Composite MLS® HPI rose by 9.7% y-o-y in October 2017, representing a further deceleration in y-o-y gains since April and the smallest increase since March 2016. (Chart B)

The deceleration in price gains largely reflects softening price trends in Greater Golden Horseshoe housing markets tracked by the index.

The y-o-y increase in the national single-family benchmark home price diminished further, continuing the trend in place since May 2017 and making it the smallest y-o-y increase since March 2015.

Apartment units again posted the largest y-o-y gains in October (+19.7%), followed by townhouse/row units (+13.2%), one-storey single family homes (+6.3%), and two-storey single family homes (+5.8%).

Benchmark home prices were up from year-ago levels in 11 of the 13 markets tracked by the MLS® HPI.

After having dipped in the second half of last year, benchmark home prices in the Lower Mainland of British Columbia have recovered and now stand at new highs (Greater Vancouver: +12.4% y-o-y; Fraser Valley: +17.3% y-o-y).

Benchmark home price increases have slowed to about 14% on a y-o-y basis in Victoria, while still running at about 19% elsewhere on Vancouver Island.

Price gains slowed further on a y-o-y basis in Greater Toronto, Oakville-Milton and Guelph; however, prices in those markets remain well above year-ago levels (Greater Toronto: +9.7% y-o-y; Oakville-Milton: +8.3% y-o-y; Guelph: +13.2% y-o-y).

Calgary benchmark prices remained just inside positive territory on a y-o-y basis in October (+0.3%), while prices in Regina and Saskatoon were down compared to last October (-1.7% y-o-y and -4.1% y-o-y, respectively). (Due to a technical issue, MLS® HPI data for Regina and Saskatoon were recalculated from July 2017 onward).

Benchmark home price growth accelerated in Ottawa (+6.6% y-o-y overall, led by a 7.2% increase in two-storey single family home prices), Greater Montreal (+5.7% y-o-y overall, led by a 7.7% increase in prices for townhouse/row units), and Greater Moncton (+5.9% y-o-y overall, led by an 8.8% increase in one-storey single family home prices).

Ottawa and Greater Montreal recorded their biggest y-o-y price gains since October 2010 and April 2011, respectively.

The MLS® Home Price Index (MLS® HPI) provides the best way of gauging price trends because average price trends are prone to being strongly distorted by changes in the mix of sales activity from one month to the next.

The actual (not seasonally adjusted) national average price for homes sold in October 2017 was just under $506,000, up 5% from one year earlier. The national average price is heavily skewed by sales in Greater Vancouver and Greater Toronto, two of Canada’s most active and expensive markets. Excluding these two markets from calculations trims more than $120,000 from the national average price (to just above $383,000).

– 30 –

PLEASE NOTE: The information contained in this news release combines both major market and national sales information from MLS® Systems from the previous month.

CREA cautions that average price information can be useful in establishing trends over time, but does not indicate actual prices in centres comprised of widely divergent neighbourhoods or account for price differential between geographic areas. Statistical information contained in this report includes all housing types.

MLS® Systems are co-operative marketing systems used only by Canada’s real estate Boards to ensure maximum exposure of properties listed for sale.

The Canadian Real Estate Association (CREA) is one of Canada’s largest single-industry trade associations, representing more than 120,000 REALTORS® working through some 90 real estate Boards and Associations.

Further information can be found at http://crea.ca/statistics.

For more information, please contact:

Pierre Leduc, Media Relations

The Canadian Real Estate Association

Tel.: 613-237-7111 or 613-884-1460